A credit score, known formally as a CIBIL Score in India, is a numerical expression of your creditworthiness based on your credit history. This score provides lenders with a means of assessing the risk involved in lending to you.

What is a Credit Score?

A credit score is a three-digit figure usually between 300 and 900 that reflects your money reliability. The higher the score, the more reliable you appear to a lender.

How Does a Credit Score Work?

Credit bureaus, such as CIBIL, collect information on your financial behavior, including loan repayments and credit card usage. The bureaus analyze that information to create your credit score.

Importance of a CIBIL Score

Your CIBIL Score is important for the following reason:

- It impacts whether your loan or credit card applications are approved or rejected.

- It determines what interest rates you may receive.

- Higher scores give you a better chance for financial opportunities.

How to Check CIBIL Score for Free?

- You can check your CIBIL Score free by:

- Using the free score function on the official CIBIL website.

- Using trusted financial services such as SBI General, Paisabazaar, or the free portals on the CIBIL website.

- You can receive instant reports online in a matter of minutes by applying for a report.

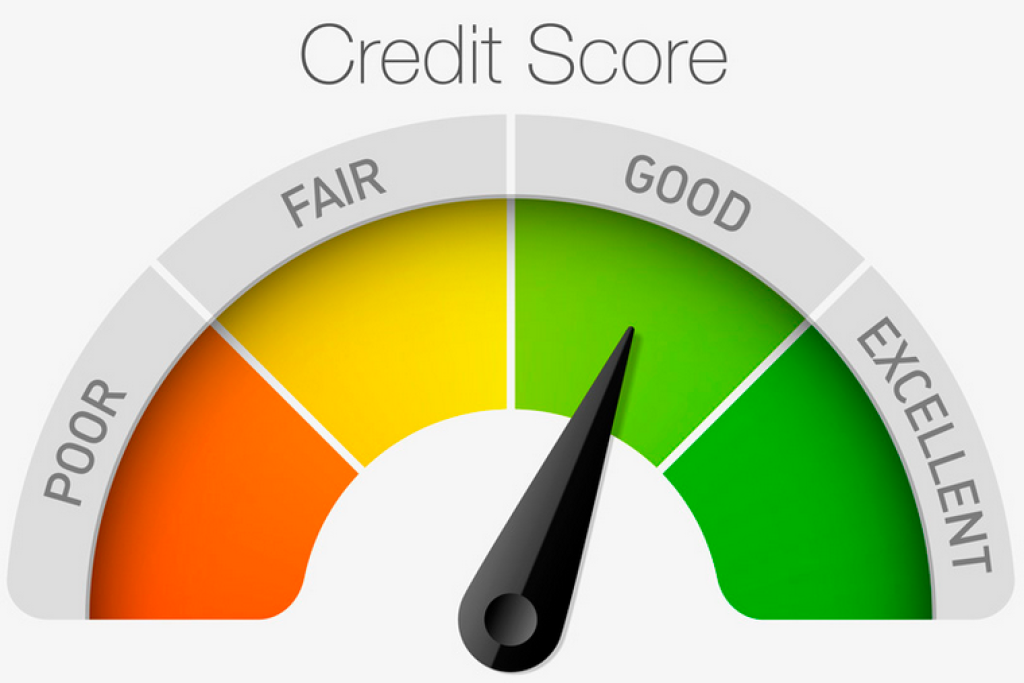

What is a Good CIBIL Score?

A ‘Good’ CIBIL Score typically refers to a score of 750 or higher, a score of 700 to 750 is considered ‘Fair’, and anything below 700 is considered a higher risk.

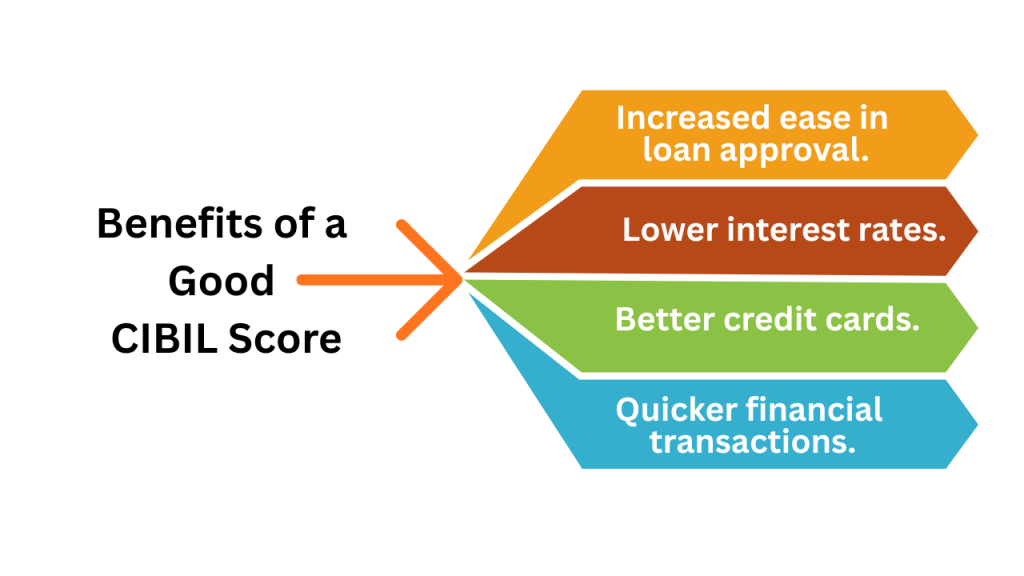

Benefits of a Good CIBIL Score

5 Factors that Affect Your CIBIL Score

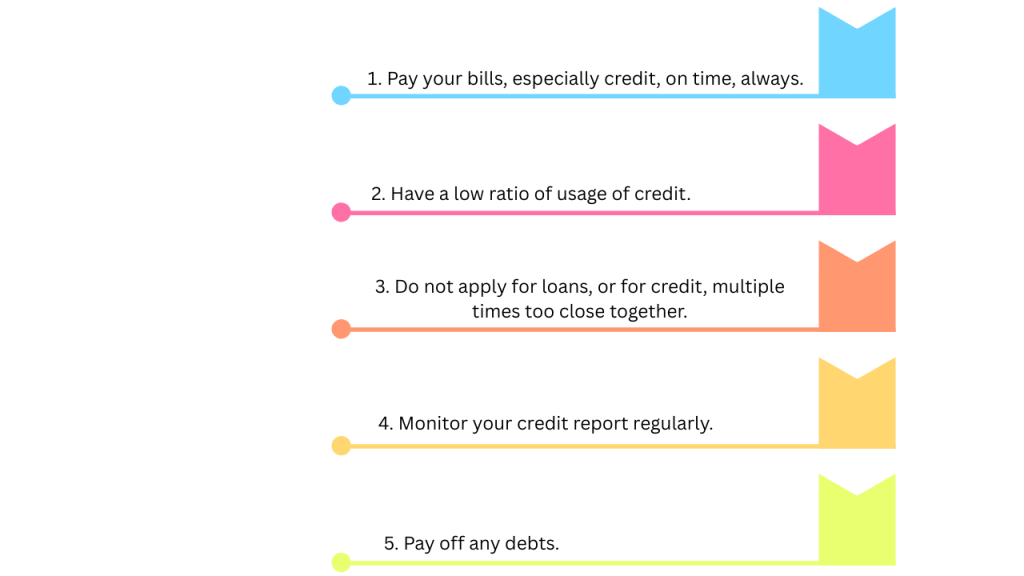

- Payment History: Pay on time, and you will eventually improve your credit history.

- Credit Utilization: The ratio of credit you’re using to availability.

- Length of Credit History: The longer the better.

- Types of Credit: Mix of secured and unsecured debt.

- Credit Inquiries: Too many loans will usually affect your score negatively.

How Your CIBIL Score is Calculated?

The CIBIL Score is calculated by a random algorithm that incorporates credit history, on-time payment history, the total amount of debt, and patterns of your credit usage.

Reasons for a My CIBIL Score

Payments that are delayed or missing.

- A high ratio of usage of credit.

- Frequently applying for loans or credit.

- Defaults or write-offs.

- Too little or no credit history.

How To Improve Your CIBIL Score?

What Information Is Not Used In My CIBIL Scores?

- Your income or salary.

- What type of job you have.

- Your balances in the bank.

- Your spending habits.

Why Do I Have Different CIBIL Scores

Different banks may get a credit score slightly different. CIBIL may change and score updates a lot, and the samples CIBIL selects may be very close but not the same time latency.

What Do I Do If I Do Not Have A CIBIL Score?

If you have never applied for credit, you likely have no score. The first thing you should do is likely, apply for a secured credit card, or small personal loan to get the account and start a score.

Why Did My CIBIL Score Change?

CIBIL can change your score if there are updates from your credit behavior, payments, your new loans, and if there were errors in the reporting.

Monitor Your Credit Report and Score

Make it a habit to regularly review your credit report to verify that it is accurate and to uncover any fraud quickly. You can obtain one free credit report from each of the major credit bureaus once each year (Equifax, Experian, TransUnion), or more frequently than that by using a service such as CIBIL.

Can I Actually Have a 900 Credit Score?

900 is the highest score there is, meaning it indicates you exhibit perfect credit behavior. It is possible, although unlikely, to achieve an excellent credit history.

Is 700 a Bad CIBIL Score?

700 is generally considered to be fair, but it is better to strive for a score 750 or higher to help in receiving favorable terms on a loan.

Is 670 a Good CIBIL Score?

670 is below-average and could make receiving loans difficult or rather costly due to the lender perceiving you as a higher risk.

What is CIBIL Report?

A document detailing your personal credit history, loans, credit cards, payment history, inquiries, and score.

What Do I Get in My CIBIL Report? Personal information.

- Summary of credit accounts.

- Payment history.

- Credit inquiries.

- CIBIL Score.

Why Should I Check my CIBIL Score & Report?

To check accuracy, detect fraud, and understand my credit health before applying for loans.

Can CIBIL delete the report?

CIBIL only makes updates based on the information provided to it by lenders; it does not delete records without reason.

What Do I Do If I See There is Something Wrong With My CIBIL Report?

Raise a dispute immediately through the CIBIL website, or customer service.

How Can I Dispute an Inaccuracy if I Already Have an Account for CIBIL?

Log into the CIBIL account and go to disputes and follow the process to raise corrections.

How Often Should I Check My CIBIL Score?

At a minimum once every 3 to 6 months or before applying for a credit.

How Do I Improve My CIBIL Score?

Pay payments on time, reduce outstanding debt, maintain a mix of credit, and do not apply for too many credit card inquiries.

Master Your Credit Health: Get a Free Credit Score Check!

FAQ for Check Your CIBIL Score Free

A CIBIL Score is a three-digit number between 300 and 900 that summarizes your creditworthiness based on your credit history. It is issued by Credit Information Bureau (India) Limited (CIBIL), a leading credit bureau in India.

It is calculated using multiple factors including your repayment history (35%), credit utilization (30%), length of credit history (15%), recent credit inquiries (15%), and credit mix (10%). Timely payments and a healthy credit mix improve the score.

Lenders use it to assess your eligibility for loans and credit cards. A good score increases chances of approval, offers access to better loan amounts, and helps secure lower interest rates.

A score above 750 is considered good or excellent, leading to smooth loan approvals and better financial products. Scores below 625 are considered low and may result in loan rejections or higher interest rates.

You can obtain a free credit score and report from the official CIBIL website or from authorized partners such as SBI General and Paisabazaar through their free services.

Main factors are timely payment of dues, the ratio of credit used to credit available, length of credit history, types of credit accounts, and the number of recent loan or credit card applications.

Yes, the score is updated frequently based on changes in your credit behavior, such as new loans, timely or missed payments, and credit utilization changes. Recent RBI rules mandate lenders to update data twice a month

The maximum score is 900, representing a very strong credit profile, but scores over 800 are generally considered excellent and rare.

A score of 700 is fair and may qualify you for loans but possibly at higher interest rates or with limited options compared to scores above 750.

If you don’t have a credit history or score, start building credit by responsibly using credit cards or loans. No credit history results in a score of -1 or zero.

It is recommended to check at least once every 3 to 6 months or before applying for any loan or credit card to detect errors or unauthorized activity early.

Yes, if you find inaccuracies such as duplicate accounts or incorrect payment history, you can raise a dispute on the CIBIL website after logging into your account.

No, checking your own score is a soft inquiry and does not impact your credit score negatively.

CIBIL updates records only based on information shared by lenders. It does not arbitrarily delete data but can correct errors after disputes are resolved.