Equated Monthly Instalment, or EMI for short, is a fixed monthly payment that borrowers make to lenders to cover principal and interest on loans and large purchases.

What is EMI?

The agreed-upon amount that borrowers pay lenders on a regular basis (typically monthly) over a predetermined loan period is known as the EMI. The most common way to pay back loans, including personal, auto, and home loans, is through installment plans (EMIs), which each include a portion of the principal and any applicable interest.

Read also : How to Check UTI PAN Card Status Online – Step by Step Guide

Importance of EMI

By dividing repayments into manageable amounts, EMIs help make expensive purchases affordable. This helps borrowers better manage their spending and avoid financial strain, enabling them to obtain necessary goods or services without having to make large, upfront payments.

How Does EMI Work?

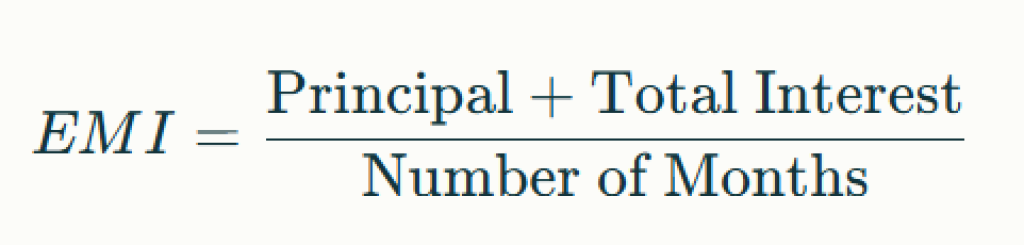

The financial institution adds interest to the principal when approving a loan to determine the total amount owed. Fixed EMIs are distributed over the repayment period as a result of dividing this amount by the number of installments (tenure). Unless the interest rate is floating, the borrower’s monthly outflow stays the same for the duration of the loan.

Two Ways Interest is Calculated on EMIs

Either the Reducing Balance Method or the Flat Interest Method are commonly used to calculate interest on EMIs:

- The flat interest method computes interest on the entire principal over the course of the term.

- Reducing Balance Method: Following each repayment, interest is computed on the remaining principal.

Flat Interest Method

The formula is:

Where interest is calculated

This method usually results in higher overall interest payments.

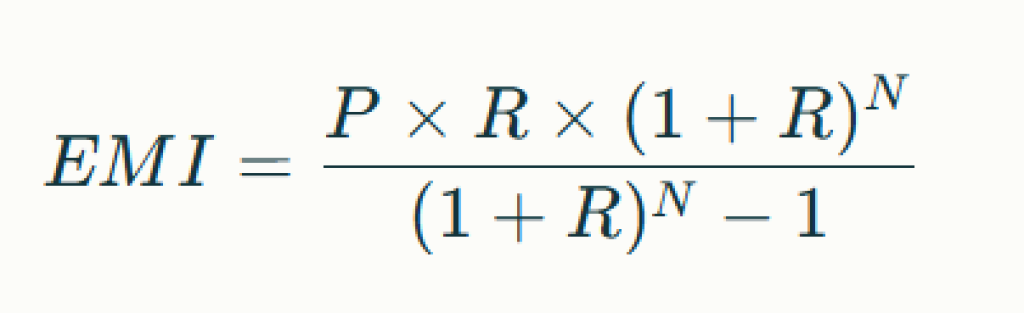

Reducing Balance Method

The formula is

Where:

- PP = Principal amount

- RR = Monthly interest rate (annual rate divided by 12)

- NN = Number of EMIs

Interest is charged on the outstanding principal post each payment, resulting in lower total interest outflow as the principal decreases over time.

Types of EMIs

Two EMI payment plans are typically available for loans:

- EMI in Arrears (Standard EMI): Principal and interest are included in each payment, which is made at the conclusion of each period.

- EMI in Advance: Just the principal is paid in the first EMI, which is made at loan disbursement. Since the upfront payment is subtracted and subsequent EMIs comprise both principal and interest, this lowers the disbursed principal.

Read also : Check Your CIBIL Score Free

Components of EMI

Each EMI has two key parts:

- Principal: Portion of the loan amount repaid.

- Interest: Cost paid for borrowing funds.

Over time, the interest component in each EMI decreases, while the principal component increases.

Factors Affecting EMI Amount

How EMI Helps in Financial Planning

By providing predictability, EMIs assist borrowers in creating monthly spending plans and preventing unforeseen financial strain. Frequent payments raise credit scores and foster sound financial practices, which makes it simpler to obtain credit in the future.

EMI vs Monthly Instalment – What’s the Difference?

Pros and Cons of Choosing EMI

Pros:

- Enables access to high-value products/services

- Predictable monthly payments, easier budgeting

- Improves credit history with regular repayment

Cons:

- Leads to long-term financial commitment

- Can attract higher interest costs over tenure

- Missed payments can hurt credit scores

How to Buy Products on Easy EMIs

Many retailers and lenders offer products on EMIs, either with no-cost (zero interest) EMI options or with standard interest rates. Products can be bought using credit cards, EMI cards, or via lender agreements. Upfront eligibility checks, documentation, and agreement on tenure/interest rate are required. Always compare interest rates, processing fees, and total cost before opting in.

Read also : Xiaomi 15T Pro Review: Price, Specs, Camera & Features in 2025

Final Thoughts

EMI is a versatile and convenient repayment tool, making aspirations more affordable and manageable. Understanding the nuances of EMI calculation, types, and impact on finances empowers borrowers to make informed decisions, balance budgets, and build strong credit profiles.

EMI stands for Equated Monthly Instalment.

Loan amount, interest rate, tenure, down payment, credit score, EMI type.

Arrears: paid at end of period, includes full principal + interest. Advance: first EMI paid upfront, deducts principal.

Reducing balance generally results in lower overall interest paid compared to the flat rate.

Yes, missed payments incur penalties and affect credit scores.

Yes, some lenders offer EMI in advance, which lowers the principal and subsequently the interest burden.